While Earned Wage Access (EWA) has been a buzzword for years, it’s still a misunderstood concept. Most people understand the idea of accessing wages before payday, but the regulations and mechanics behind it are far more complex. There are multiple ways to implement an EWA program, each with its own compliance and risk implications.

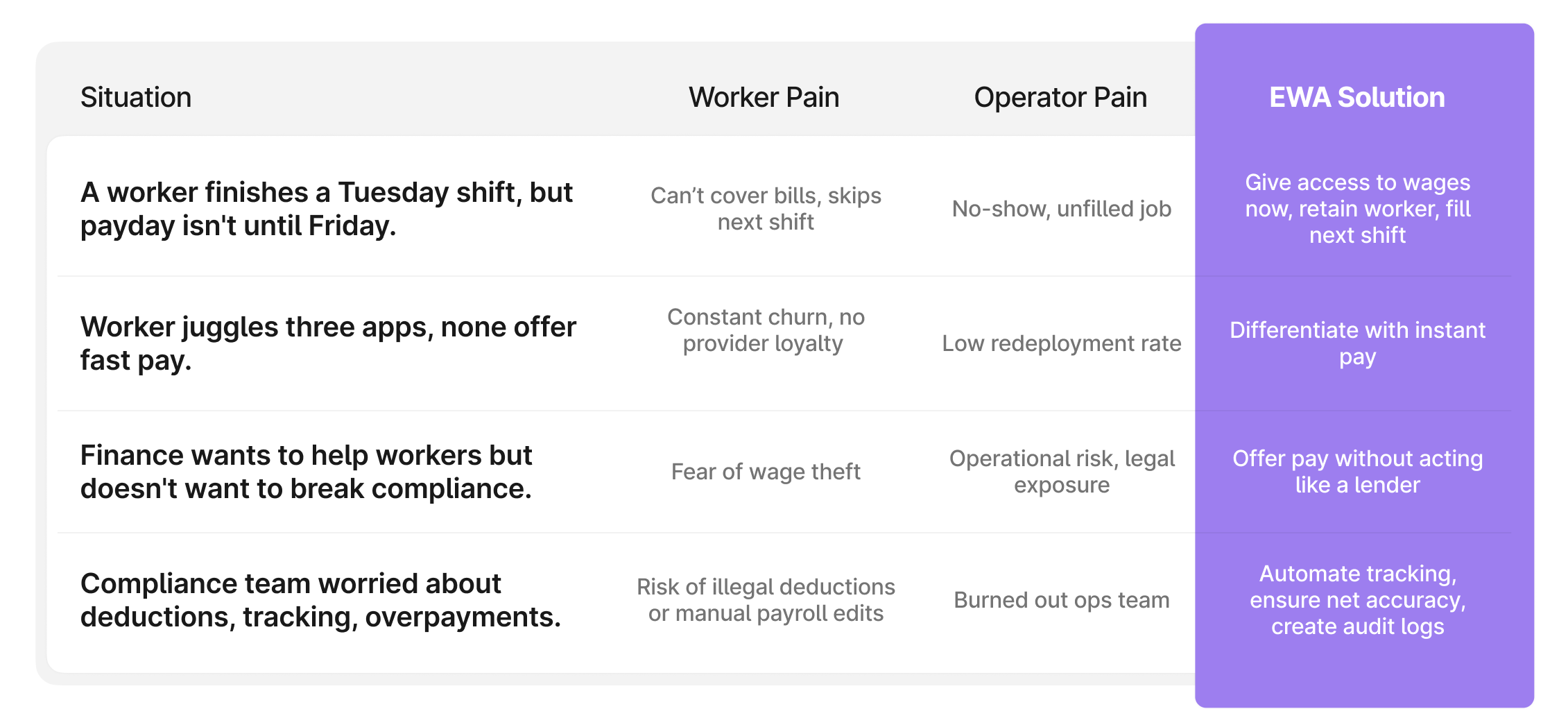

We built this guide because most staffing operators don’t realize the compliance landmines hiding inside EWA. Did you know a single payroll deduction can trigger a wage theft claim in California? Or that third-party wage advances in New York may now be classified as loans? Or that most “free EWA” products still include hidden tips or delivery fees? This isn’t theoretical. It’s happening.

Earned Wage Access is no longer a “nice-to-have.” It’s a competitive necessity—especially in high-churn, high-volume industries like staffing.

But here’s the catch: most EWA models are built for speed, not compliance. They skirt wage laws. They charge workers fees. They’re increasingly being reclassified as credit under evolving state and federal rules. And if you’re not careful, your program could put your business at legal risk.

If you’re a staffing company looking to improve worker satisfaction and differentiate yourself by offering EWA, this guide has everything you need: how each model works (and the risks they carry), which rules apply in the states you operate in, and what it takes to deliver instant pay—without instant liability.

with applicable wage and hour laws, which can vary significantly by state.

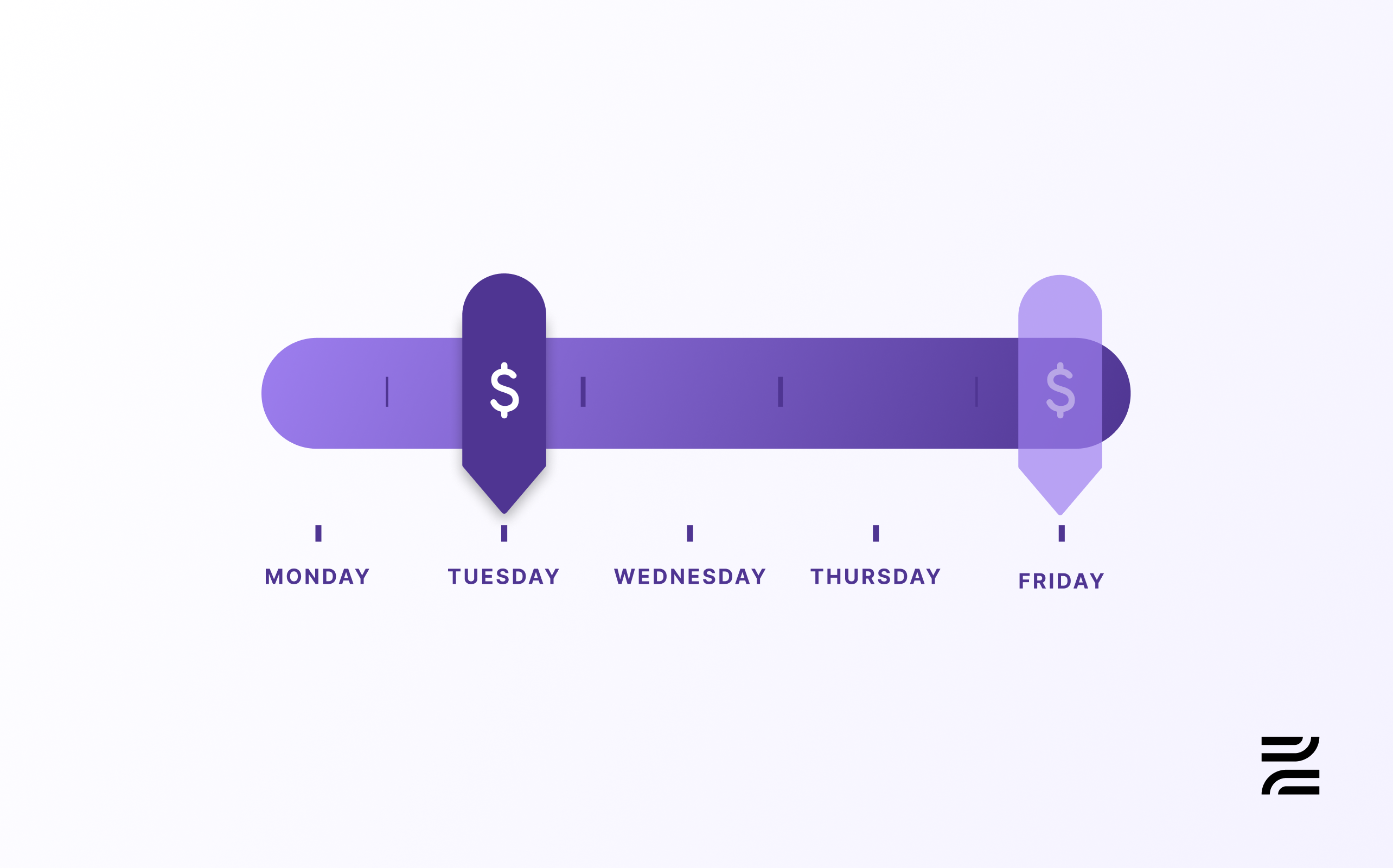

Staffing companies don’t implement EWA to sound progressive.

They implement it because they’re losing workers. Bleeding cash on turnover. Scrambling to fill shifts.

Your workers aren’t comparing your pay policies to your competitors. They’re comparing it to different ways to access money now. If you don’t offer a clean, fast, compliant way to deliver it—they’ll leave.

If you do offer EWA, the benefits are big for you and your workers.

As of January 2025, 65% of Americans live paycheck-to-paycheck. For many Americans, the cost of bills and necessary expenses like electricity and groceries have only increased—78% of all consumers reported experiencing at least one bill increase in the past year. The lack of available funds can impact a person’s ability to cope with unforeseen cirsumtances—nearly half of all Americans can’t afford an unexpected expense over $400.

These statistics underscore the financial vulnerability many individuals face. Earned Wage Access (EWA) offers meaningful advantages to employees whose quality of life is directly tied to the immediacy of their wages. For employers, especially in fast-paced industries like staffing, EWA represents an opportunity to retain talent by helping employees alleviate financial stress.

While the benefits are big, if you offer EWA the wrong way, you could end up in a regulatory mess.

The compliance, operational, and financial implications of an EWA program depend heavily on the model used. Here’s a breakdown of the three major models and how they differ:

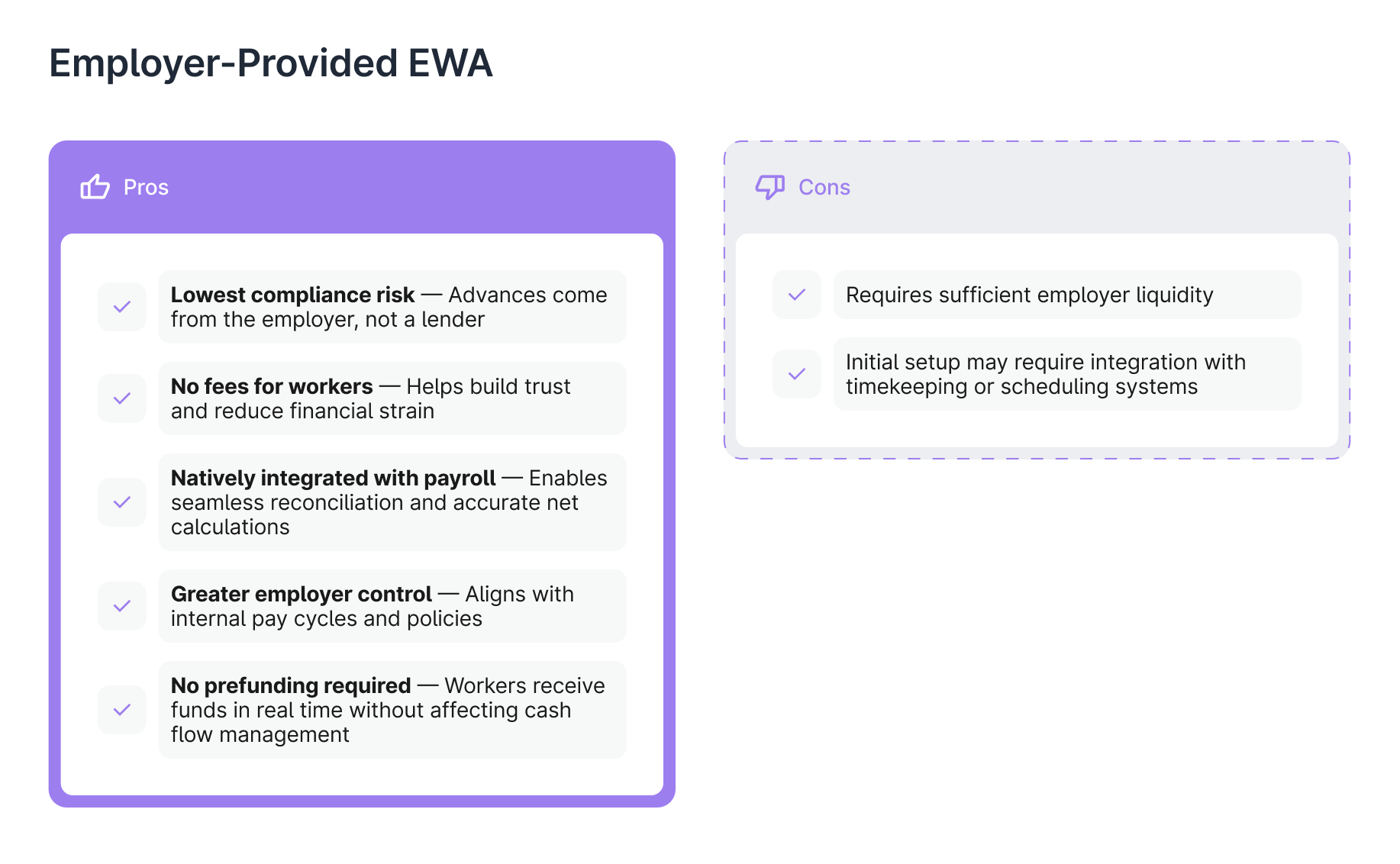

The employer directly advances wages to the employee from its own funds, often using a provider only for software infrastructure. No third-party lender is involved.

Employer-provided EWA model means the employer—not a third party—funds wage advances directly. A payroll software solutions acts as the infrastructure layer, enabling accurate payroll data tracking, gross-to-net calculations, payment processing, and real-time reconciliation. While the payroll software can facilitate delivery of funds to workers (e.g., via instant pay to debit card), it does so on behalf of the employer. Because the employer is the funder, workers are not charged fees, and the model avoids being classified as credit under laws like Regulation Z. This structure gives staffing companies maximum control, low compliance risk, and the ability to offer a high-trust benefit to their workforce.

While EWA seems simple on the surface—workers get paid earlier than the standard payroll cycle—successful EWA implementation relies on deep payroll integration, strategic adherence to compliance obligations, and a clear understanding of the program used. These elements determine the user experience, operational complexities, and legal implications.

EWA solutions typically integrate with time-tracking and payroll platforms to pull real-time or near-real-time data about hours worked and wages earned. This data enables:

Here’s how it works:

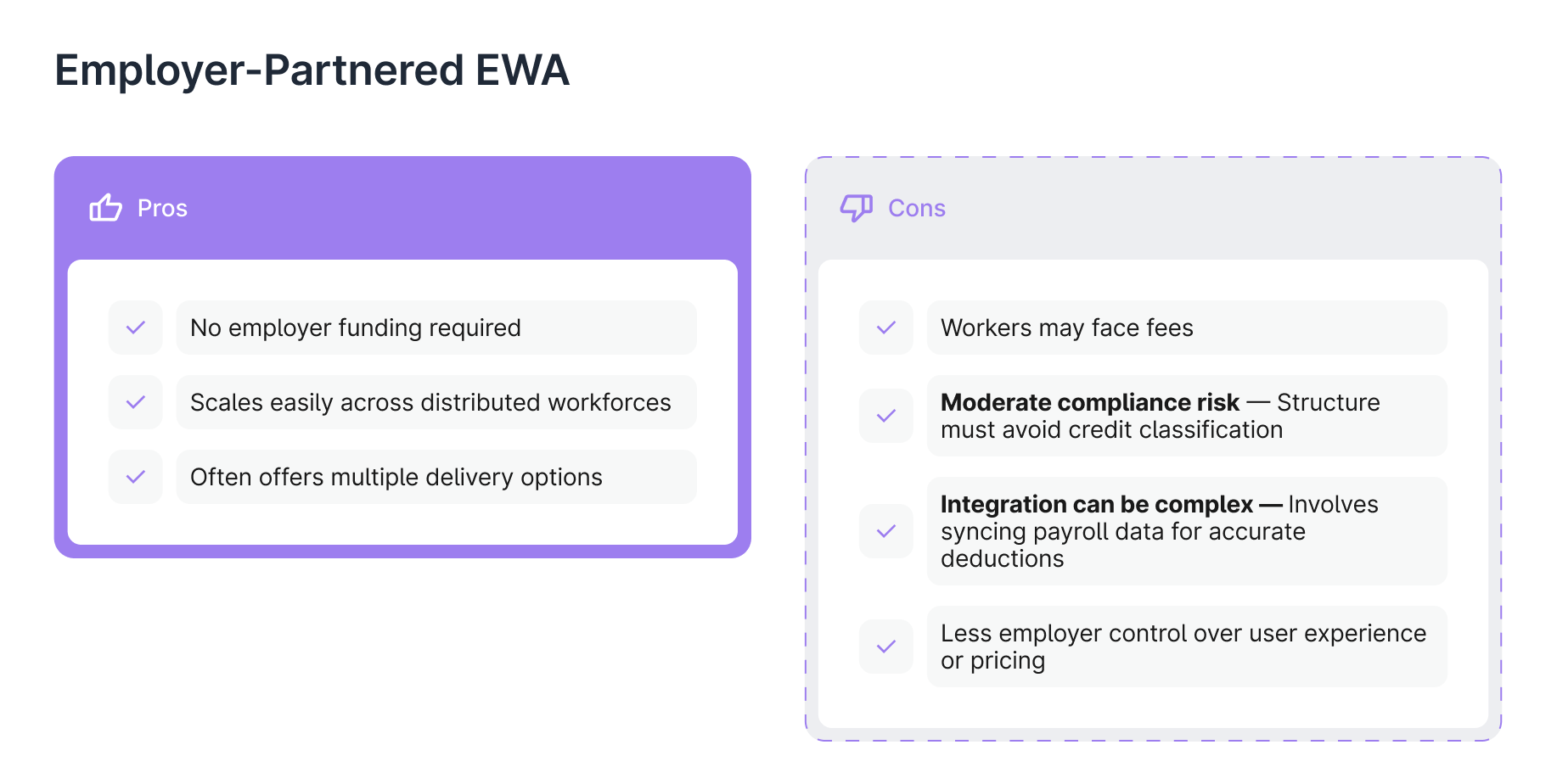

Many third-party Earned Wage Access (EWA) providers operate under an employer-partnered model where the provider advances funds to workers ahead of payday, then recoups the amount via payroll deduction. These setups typically rely on deep integrations with employer payroll or time-tracking systems to verify earned wages. While some offer a no-cost option, workers are often nudged toward faster delivery methods that come with fees or “tips.” Though structured to avoid triggering credit regulations—by avoiding interest, credit checks, or mandatory repayment—these models still introduce compliance gray zones and can create a fragmented worker experience.

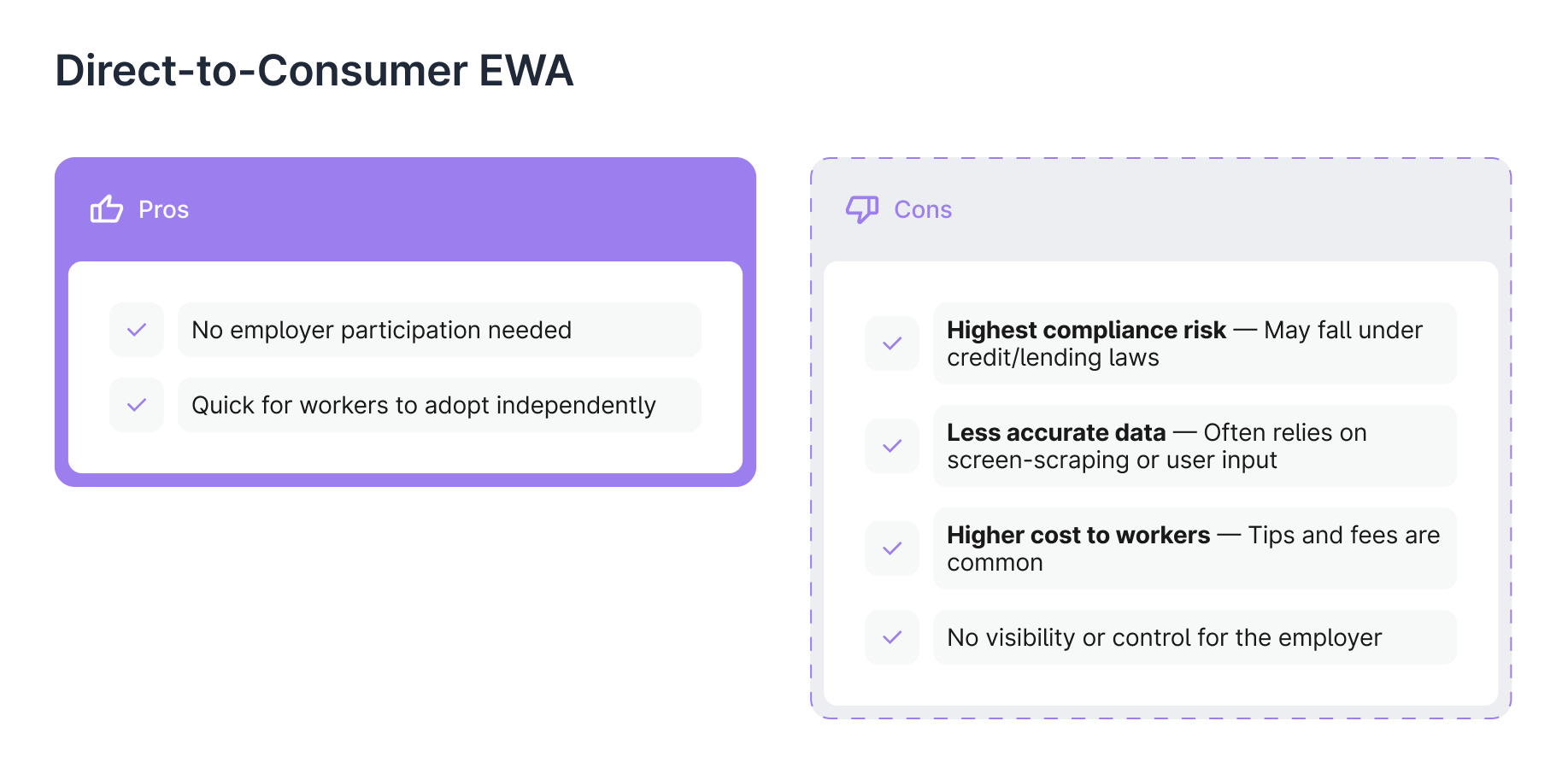

The direct-to-consumer Earned Wage Access model bypasses employers entirely. Workers download a consumer-facing app, connect their bank account, and log into their payroll system directly—often using screen-scraping tools. These providers estimate earnings, advance funds to the worker, and automatically withdraw repayment on payday. While some market themselves as tip- or fee-optional, the repayment structures can blur the line between EWA and consumer credit—raising legal and regulatory risks under lending laws. Because employers aren’t in the loop, these models also offer no visibility or control to staffing companies, and can undermine a unified worker experience.

The answer depends entirely on the EWA model. The employer-provided model has the employer funding; while the others are funded by third parties. Understanding who fronts the money, and when repayment occurs, can help staffing companies make smarter financial and compliance decisions.

In this model, the employer is the funder. Workers access a portion of their net earned wages early, and the advance is reconciled on payday.

A third-party provider funds the wage advance and recoups the money via payroll deduction on payday.

The provider offers wage access independently of the employer, using banking credentials or payroll login credentials provided by the worker.

Earned Wage Access (EWA) can deliver real value to workers and differentiate your firm—but only if it’s designed with compliance in mind. Because federal guidance is still evolving, staffing firms must navigate a patchwork of state wage laws, deduction rules, and data privacy regulations. Below are the key areas to get right:

If your EWA model uses payroll deductions to recover advances:

EWA requires sharing sensitive payroll and banking data. You and your vendor must:

How you structure fees—and whether they’re charged to the worker—can determine whether your EWA program is treated as a loan or subject to credit regulations.

Common EWA Fee Types:

In 2020, the Consumer Financial Protection Bureau (CFPB) issued guidance suggesting that certain EWA products that did not charge fees and were non-recourse (i.e., no obligation to repay) were not considered credit under Regulation Z (Truth in Lending Act).

In July 2024, the CFPB proposed a new interpretive rule indicating that many EWA programs should be treated as credit. This would mean:

In January 2025, this guidance was officially rescinded, creating uncertainty in how EWA programs will be treated at the federal level. Without federal guidance, state-level legislation has become the primary source of regulatory guidance for Earned Wage Access. However, individual state laws vary widely on licensing, disclosure fees, and wage deductions. Therefore, for staffing companies looking to offer EWA, it is essential to conduct a state-by-state compliance review to avoid regulatory risk.

For staffing companies, especially those operating in multiple jurisdictions, compliance challenges can quickly become complex. Both the implementation and execution of EWA must be done strategically so as not to cross regulatory lines.

If your EWA program is classified as credit, you are required to comply with:

Key triggers that might lead regulators to classify your program as credit:

If your EWA model relies on payroll deductions to recover advances (typical in employer-partnered programs), you must comply with:

Mistakes here aren’t just regulatory issues, they can also trigger wage theft claims.

Several states, including Arkansas, South Carolina, Nevada, and Utah have enacted laws requiring employers to:

If you use a vendor who adds fees, tips, or “optional donations,” you could be implicated in a structure that runs afoul of local law.

As of mid-2025, five states have passed EWA-specific legislation, and 16 more have bills proposed. Requirements range from:

EWA providers should not only be aware of the legal risks, but the operational ones as well. Even the most well-designed EWA model can fail if:

The number one question staffing companies have when considering establishing an EWA program is: what happens if I pay too much? It’s a worthwhile question because even with strong systems in place, errors happen. A worker might get paid for an unapproved shift, or a disbursement might exceed what they actually earned. These mistakes need to be reconciled carefully because, in an Earned Wage Access program, once wages have been disbursed, it’s not always straightforward to get them back.

Overpayments in EWA typically stem from:

These errors are rare but when they do happen, recouping the funds can trigger legal and compliance risks.

It depends on the state. While some states allow employers to correct overpayments by deducting from future paychecks, others impose strict limits or require employee consent. For example:

Failing to follow state rules can result in wage theft claims, penalties, or lawsuits—even if the error was honest.

In many jurisdictions, you can’t deduct anything from a worker’s pay without written consent—including to fix an overpayment. That’s why it’s critical to:

Pro tip: Employer-Provided model can have an EWA system that includes the following features that help prevent double payments and ensure compliant deductions so overpayments are rare by design:

The safest EWA programs:

If you do need to recover funds, consult legal counsel and ensure you’re following the rules in every state you operate in.

Rolling out Earned Wage Access isn’t just about flipping a switch—it’s about aligning your payroll systems, compliance processes, and worker communications to deliver a seamless, secure experience. Here’s how to get started:

Before anything else, decide which EWA structure works best for your business:

Tip: Employer-Provided EWA offers the cleanest compliance path for W-2 staffing, with the fewest legal risks and the best user experience.

To enable real-time pay:

If the answer to either of these questions is no, upgrade your back office before adopting an EWA program.

Start small and iterate:

Track metrics like:

Work with your provider to:

Reminder: Compliance varies widely. Some states allow employer-paid fees, others prohibit any fees to workers. Your provider should hard-code these restrictions into their system.

Automated Compliance: Some providers have a compliance engine automatically detects the state jurisdiction for each employer and worker, configures permitted disbursement options, and ensures only compliant choices are made available to workers. Fee-free options are always available, and restrictions (like no worker-paid fees in NY or NV) are enforced at the system level—no manual oversight required.

Think strategically about your internal communications strategy. It’s important to:

Not sure which EWA model is right for your business? Let’s figure it out together.

Zeal offers 1:1 consultations to help staffing firms choose the best Earned Wage Access model based on their unique structure, client mix, and worker needs. We’ll walk you through:

EWA doesn’t have to be a legal risk, a payroll mess, or a money pit. When done right, it’s a revenue driver, a retention tool, and a reason clients choose you over the next firm.

Schedule a consultation: https://www.zeal.com/contact-us

Earned Wage Access allows workers to access wages they’ve already earned before their scheduled payday. In staffing and workforce platforms, EWA is typically integrated directly into payroll and time systems so workers can receive funds after shifts are completed and approved—without changing pay frequency or classification.

They’re related but not identical:

Many modern platforms combine EWA with instant pay rails.

It depends on how the program is structured.

Employer-provided or employer-partnered EWA programs—where workers access wages they’ve already earned and repayment happens automatically through payroll—are generally considered lower risk than third-party, fee-based models that advance funds independently.

Program structure matters more than the label.

Yes, if EWA is not integrated correctly. Key risks include:

Payroll-native EWA models reduce these risks by embedding access directly into compliant payroll workflows.

No. Properly implemented EWA does not replace or alter statutory pay frequency.

Workers still receive full payroll on their regular payday; EWA simply allows access to a portion of earned wages in advance.

In a payroll-native model:

This avoids manual adjustments, spreadsheets, or off-cycle runs.

Yes—but workflows differ:

Platforms should support both without forcing them into the same workflow.

Key requirements include:

Bolt-on solutions often introduce risk at scale.

Share this:

Zeal is a financial technology company, not an FDIC insured depository institution. Banking services provided by Bangor Savings Bank, Member FDIC. FDIC insurance coverage protects against the failure of an FDIC insured depository institution. Pass-through FDIC insurance coverage is subject to certain conditions.

Mastercard® Debit Card is issued by Bangor Savings Bank, Member FDIC, pursuant to license by Mastercard International Incorporated. Mastercard is a registered trademark, and the circle design is a trademark of Mastercard International Incorporated. Spend anywhere Mastercard is accepted.